Blockchain is inevitable in capital markets, but only if it respects the hard-won lessons of market structure.

Simon Yi

Co-Founder Myosin.xyz

Jan 6, 2026

For years, blockchain advocates have pitched a wholesale reinvention of capital markets. The message from Wall Street today is far more measured and far more consequential. The future isn’t about ripping out exchanges or moving equities trading wholesale onchain. It’s about using blockchain where it meaningfully improves market plumbing, without jeopardizing liquidity, anonymity, or risk management.

That distinction came through clearly at FT Partners’ recent panel on tokenization of real-world assets, featuring leaders from Nasdaq, Tradeweb, Digital Asset, Figure, and DRW. The consensus view: blockchain is inevitable in capital markets, but only if it respects the hard-won lessons of market structure.

Liquidity Is Sacred

Adena Friedman, CEO of Nasdaq, set the tone. U.S. equities markets work because liquidity is deep, centralized, and highly participatory. Fragment that liquidity across multiple chains or synthetic representations, and you undermine the very thing that makes public markets efficient.

That’s why Nasdaq is skeptical of onchain auctions. Public blockchains expose too much information, too early. Bids must remain anonymous. Market participants cannot trade if counterparties can infer intent, size, or positions in real time. This isn’t a philosophical objection, it’s a practical one. Price formation depends on private bids in the auction.

Where blockchain does make sense is post-trade. Settlement, reconciliation, ownership records, corporate actions, and voting are riddled with friction. Onchain ownership creates a clean, auditable record of who owns what, when. Onchain voting modernizes shareholder participation. Real value is created after settlement, through faster and more transparent disclosures, not through real-time transparency that enables front-running.

One Stock, One Asset

Across the panel, a shared concern emerged: multiple onchain representations of the same equity are a structural failure, not a feature.

Yuval Rooz of Digital Asset put it bluntly. If Tesla trades as five different tokens across Solana, Ethereum, Base, and Linea, liquidity fractures. Collateral efficiency degrades. Markets become thinner, which is not good for anyone. Nasdaq’s ambition to “own interoperability” for tokenized equities reflects this reality: capital markets need aggregation, not proliferation.

This also intersects with collateral. Onchain equities unlock powerful new financing use cases like stock lending, cross-collateralization, and real-time margining, but those benefits only materialize if the asset is singular, trusted, and privacy-preserving.

Speed Without Exposure

Billy Hult of Tradeweb, a veteran of fixed-income markets since the Liar’s Poker era, highlighted how far markets have already evolved. Transparency improved price discovery, but not by exposing individual trades mid-execution. The same principle applies onchain.

Blockchains can dramatically speed settlement and enable 24/7/365 markets, including for traditionally less liquid assets like residential mortgage backed securities. Speed and availability of markets are valuable. However, radical transparency is not. Transaction visibility must be tightly controlled, which is why the buy side likes to trade on NASDAQ. If everyone can see who is borrowing against which stock, or how crowded a trade is in real time, that would compromise the trade position and potentially eliminate the opportunity for the trade due to MEV attacks.

Capital Efficiency Is the Killer App

Mike Cagney of Figure offered the most concrete proof point. By tokenizing home equity lines of credit (HELOCs) onchain, Figure has eliminated roughly 150 basis points of transaction friction, $10 million in issuance at a time at first, and now issuing $1 billion of HELOCs onchain. That’s the operational leverage of blockchain technology.

DeFi, in Wall Street’s framing, isn’t about permissionless speculation. It’s about unencumbered capital, continuous financing, and better sources and uses of liquidity. Figure’s decision to issue a secondary IPO natively on Solana underscores where momentum is coming from: the buy side. Adoption won’t be led by retail traders. It will be pulled in by institutions seeking efficiency.

The Hard Problems Remain

Don Wilson of DRW grounded the discussion in reality. Most “onchain stocks” today are closer to swaps than true equities. And if markets move toward 24/7 trading, collateral and clearing must move 24/7 as well. Clearinghouses that close overnight and on weekends become systemic bottlenecks.

Default risk, Basel capital treatment, and structures like AB2 aren’t solved by code alone. Blockchain doesn’t eliminate overnight or default risk, it reshapes it. Managing that transition is the real challenge ahead.

The Bottom Line

Wall Street isn’t anti-blockchain. It’s anti-naivety.

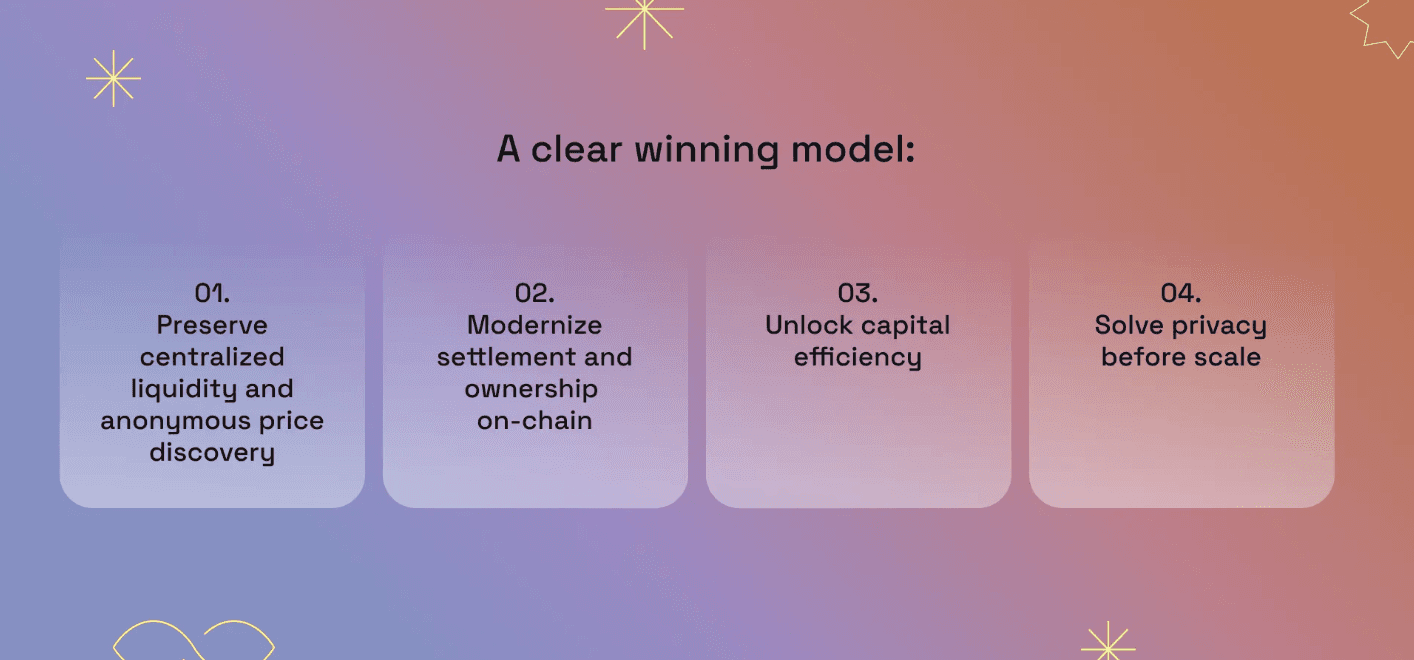

The winning model is clear: preserve centralized liquidity and anonymous price discovery, modernize settlement and ownership onchain, unlock capital efficiency, and solve privacy before scale.

The revolution won’t look like DeFi Twitter imagined, but it may quietly remake the infrastructure beneath global markets after all.